The gas station equipment market is evolving rapidly in 2026 with tightening regulations, infrastructure upgrades, and shifting demand across all regions.

Asia-Pacific Leads Global Growth

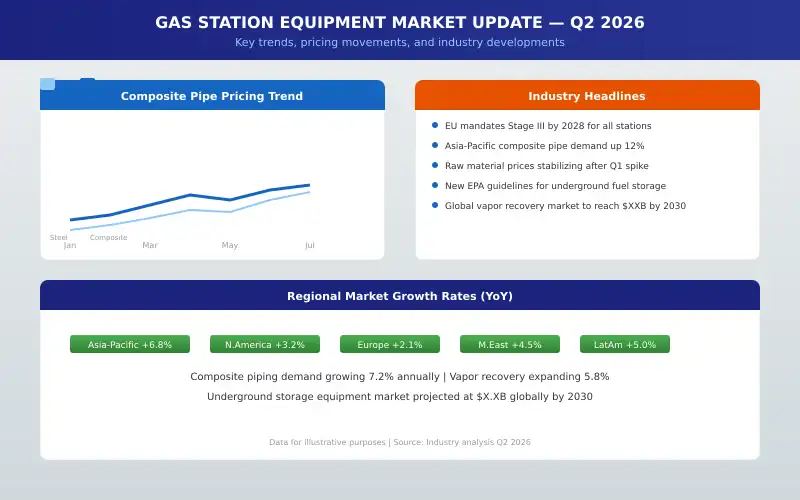

Asia-Pacific continues to dominate the global market with a 42.3% share and the strongest year-over-year growth at 6.8%. Rapid urbanization in China and India, combined with expanding vehicle ownership across Southeast Asia, is driving significant new station construction. This creates strong demand for underground composite piping, vapor recovery equipment, and monitoring systems. Local manufacturing capacity is expanding but quality-certified imported equipment remains in high demand.

Environmental Regulations Driving Replacement Cycles

Regulatory changes are the primary catalyst for equipment upgrades worldwide. The European Union has announced that Stage III vapor recovery will be mandatory for all service stations by 2028, driving a multi-year replacement cycle. New EPA guidelines in the United States are tightening requirements for underground storage system leak detection and secondary containment. These regulatory drivers create sustained demand for compliant equipment across established markets.

Composite Pipe Demand Accelerating

Underground composite piping continues to gain market share from traditional steel at an accelerating pace. Annual demand growth of 7.2% reflects the growing recognition of composite benefits among station operators. The trend is most pronounced in new construction projects, where operators are choosing composite from the start rather than retrofitting later. Major oil companies are increasingly specifying composite piping for their branded station networks.

Vapor Recovery Equipment Expansion

The vapor recovery equipment market is benefiting from both regulatory mandates and voluntary adoption by environmentally conscious operators. Stage III systems are becoming the global standard for new stations, with the market projected to grow at 5.8% annually through 2030. Technological improvements are making systems more reliable and easier to maintain, reducing a traditional barrier to adoption.

Raw Material and Pricing Trends

Raw material prices for composite pipe manufacturing stabilized in Q2 2026 after volatility in early 2026. Fiberglass and resin prices have moderated, providing some relief to manufacturers and downstream buyers. Steel prices remain elevated due to global supply constraints, narrowing the price gap between composite and steel options and accelerating the shift to composite materials.

International Trade Dynamics

Supply chain diversification continues as manufacturers establish production capacity across multiple regions. Trade policy developments, including tariff adjustments and new trade agreements, are influencing equipment pricing and availability. International quality certifications are becoming increasingly important as buyers seek equipment that meets multiple regulatory standards.

Outlook for the Remainder of 2026

The market outlook for the remainder of 2026 remains positive. Composite pipe demand is expected to continue its strong growth trajectory. Vapor recovery equipment orders remain robust across all major regions. Emerging markets in Africa and Latin America offer high growth potential as they build out fuel retail infrastructure. Station owners planning equipment investments should act promptly to secure supply chain capacity and favorable pricing.

WoHong Petrochemical monitors global market trends to provide our customers with competitive products and market intelligence. Contact us for updated information and equipment solutions.